Future Trends

|

Jan 22, 2026

7 Big Predictions For 2026–2030 (And What They Mean For You)

Seven bold predictions on health, IRL experiences, AI, SaaS, plastic, India, and LATAM that show how 2026–2030 will reshape consumers, markets, and technology.

Over the next five years, the stories that shape our lives will not just be about interest rates and stock charts. They will be about what we do with our bodies, where we spend our attention, which countries become the new centers of gravity, and how quietly the infrastructure around us changes while we are busy scrolling. Between 2026 and 2030, health turns into a status symbol, real-world experiences become the premium screen, India and parts of LATAM evolve into demand powerhouses, sustainable materials finally challenge plastic, AI business models flip toward the individual, SaaS economics get rewritten, and even the roads under our cars start to behave differently. These seven predictions are not meant to be perfect forecasts, but a map of where the ground is already starting to move and what it could mean for anyone building, investing or simply planning their next decade.

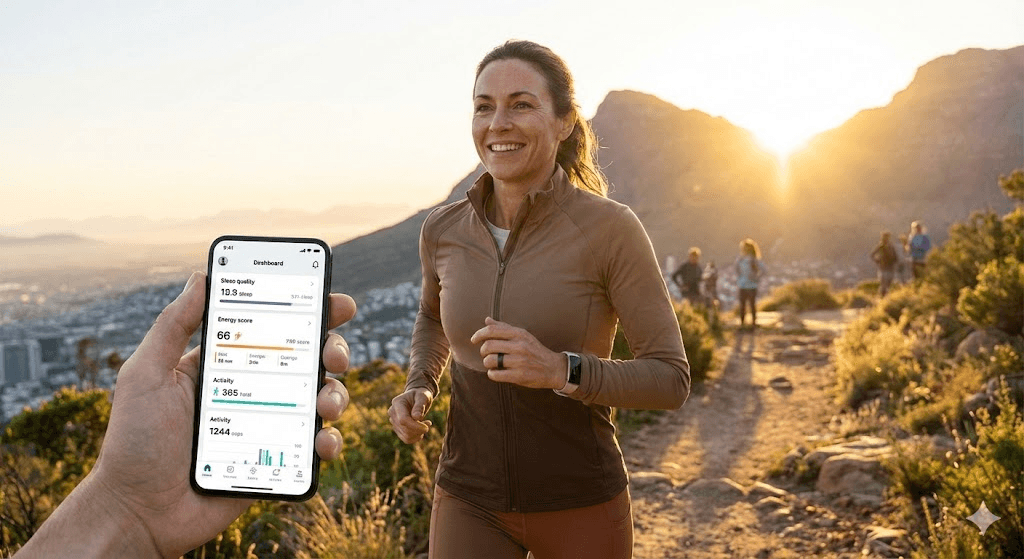

1. Healthy Is The New Wealthy

Over the next five years, health stops being a side project and becomes the main scoreboard. Status is less about what you park in your driveway and more about your energy, sleep quality, lab results and how long you can stay sharp and active. Wearables and preventive tools move from “nice to have” to daily companions as consumers treat health the way previous generations treated money.

Health becomes the most expensive thing people are willing to pay for in advance.

Spending patterns are already shifting in that direction. Fitness and wellness startups attracted billions in funding in 2025, with smart rings, metabolic trackers and at-home testing surging in adoption. Younger consumers are far more likely to invest in preventive care, longevity products and personalized feedback, and they are comfortable treating health as a continuous subscription rather than an occasional checkup. Insurance products and employers are catching up, offering incentives for sleep, movement and nutrition metrics instead of just reimbursing hospital visits.

This creates winners and losers. Companies that help people sleep better, recover faster and manage stress more intelligently will see compounding loyalty, because they become part of someone’s identity and daily routine. On the other side, industries built on self-harm and escapism are under quiet pressure. Alcohol consumption among younger cohorts is already trending lower in many markets, and as health becomes aspirational, heavy drinking looks less like fun and more like a tax on tomorrow.

Regulators and employers will accelerate this transition by tying real money to behavior. Health-linked incentives for groceries, gym memberships, coaching and diagnostics will slowly turn into a parallel economy where being healthy literally pays. By 2030, the clearest signal of wealth is not a watch that costs more, but a life that runs better.

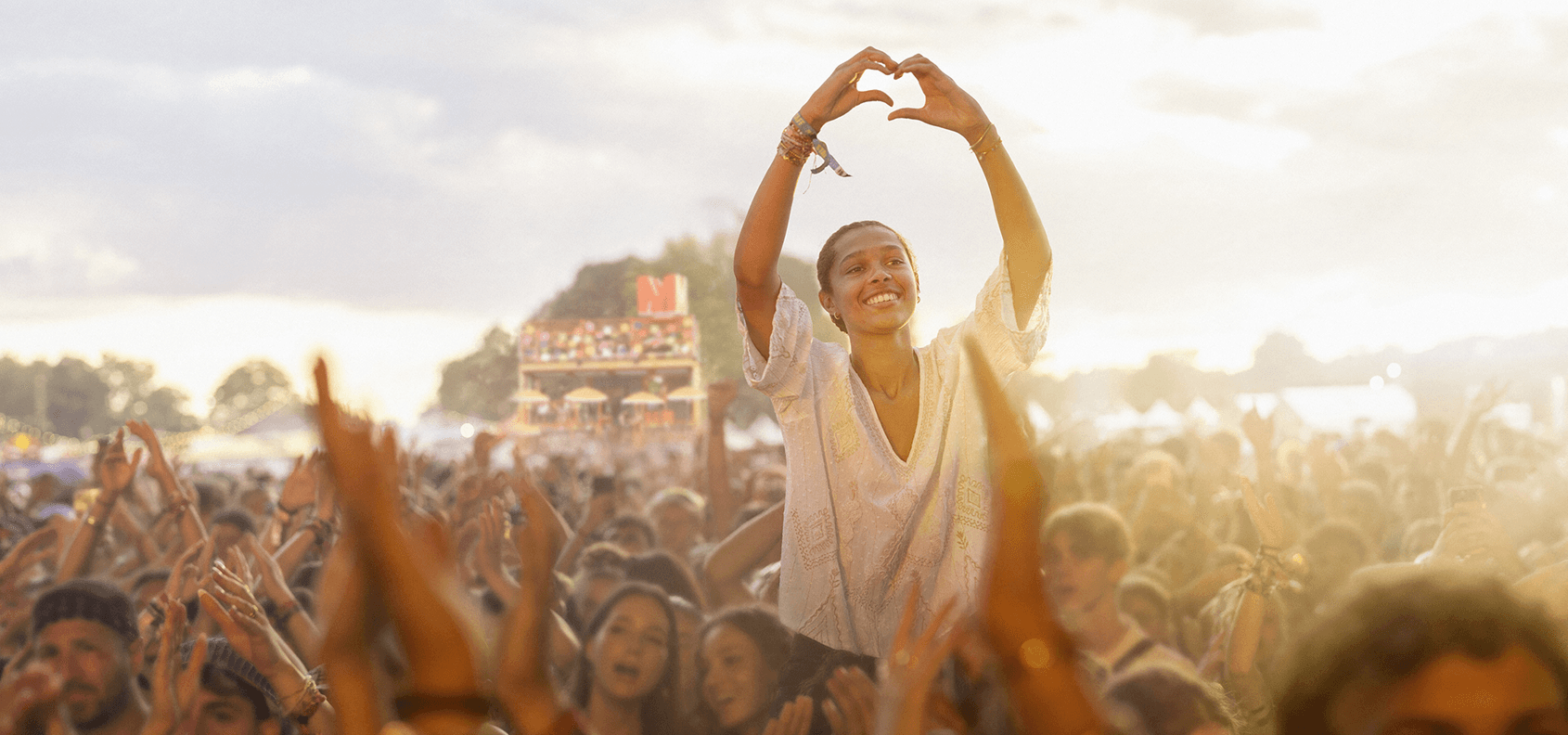

2. IRL Experiences Become The New Premium Screen

As AI makes it trivial to fabricate convincing videos, voices and images, people start to quietly downgrade the trust they place in anything that appears only on a screen. The default question becomes: “Did anyone I trust actually see this with their own eyes?” That question pushes attention and money back into live, in-person experiences.

The only content that cannot be faked is the moment you were there.

Travel, festivals, concerts, retreats, sports events and workshops benefit from this shift. Cultural tourism and festival travel are already growing faster than many other leisure categories as people chase connection, atmosphere and memory rather than another algorithmic feed. When your social circle is full of AI-polished highlights, the most credible flex is holding a ticket stub or wristband that says “I showed up.”

Online media does not disappear, but it becomes commoditized. If anyone can generate passable videos and posts in seconds, it becomes almost impossible to stand out purely through pixels. Brands, creators and educators that want to charge premium prices increasingly need to offer something that is anchored in a room, a city, a stadium or a physical community, even if the discovery happens online.

This is especially true for younger audiences. They are perfectly comfortable in digital spaces, but are also the quickest to spot when something feels over-produced or fake. Real-world experiences that are messy, improvised and a little unpredictable become more attractive precisely because they cannot be copy-pasted. The more AI fills the internet with endless content, the more valuable the few hours become where phones are in pockets and people are fully present.

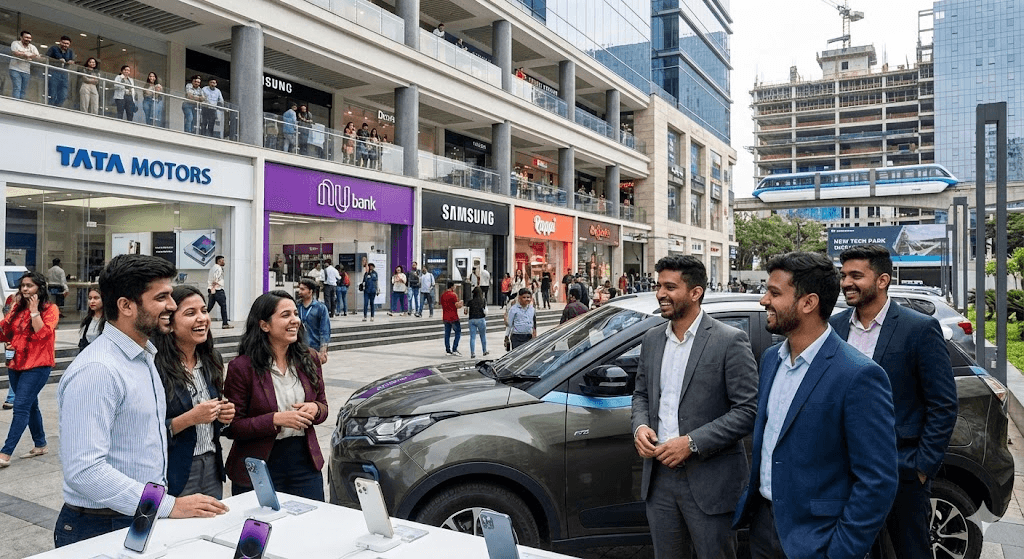

3. India And LATAM Become The New Consumer Gravity Centers

The next big story in global consumption is not happening in New York, London or Berlin. It is unfolding in places like Bengaluru, São Paulo and Mexico City. India in particular is heading into a multi-year period where a young, increasingly skilled population has more money in their pockets and more appetite for quality goods and services.

For the next decade, “product-market fit” means “India and LATAM fit.”

Surveys show that a majority of Indian consumers expect to increase household spending, especially on autos, phones and other long-cycle items, and overall consumer confidence is among the highest in the world. Reports highlight that this is not just more spending, but better spending: a shift toward premium, higher quality and more sustainable products as incomes and expectations rise. Fitch and others now see private consumption as the main driver of India’s growth through 2026 and beyond.

That changes India’s role in the global economy. Instead of being framed mainly as an outsourcing hub, India becomes one of the most attractive demand centers, pulling in global and local brands across finance, healthcare, entertainment, travel and digital services. Capital and talent follow opportunity. Startups and multinationals design products first for Indian consumers, then adapt them elsewhere, reversing the usual pattern where emerging markets get the “lite” version of Western products.

A similar, if more uneven, story plays out across Latin America. Urban middle classes in Brazil, Mexico, Colombia and others are growing in sophistication and digital fluency, even if macro and political risks remain. Over the next five years, the most interesting consumer experiments will often launch in these markets first, where demographics and hunger for upward mobility create a rare combination: large market, fast growth, and a willingness to try new things.

4. Eco-Friendly Materials End Plastic’s Monopoly

Plastic will not disappear by 2030, but its historic free pass is ending. A combination of policy pressure, consumer expectation and technical progress is finally making alternatives like mycelium, hemp, bamboo and advanced bio-composites genuinely competitive in cost and performance.

Plastic shifts from default choice to guilty pleasure.

Many of these materials are already out of the lab and into real supply chains. Mycelium-based packaging can be grown into custom shapes that protect fragile goods and then safely decompose. Bamboo and agricultural fiber blends are now used in everything from cutlery to structural boards, offering strength and durability with a far smaller environmental footprint. As scaling continues, the price gap with traditional plastics narrows, especially when you factor in waste and disposal costs.

Regulation will do the rest. Governments are under pressure to hit climate and pollution targets, and that means they can no longer ignore the billions of tons of plastic entering landfills and oceans. Expect a mix of plastic taxes, bans on specific single-use items, and extended producer responsibility schemes that make manufacturers financially responsible for the waste they create. At the same time, public money will go into large-scale cleanup and recovery projects to deal with legacy plastic that is already out there.

For companies, sticking with virgin plastic becomes less about convenience and more about risk. Input price volatility, compliance costs and reputational damage will all trend up. By contrast, early movers in bio-based and circular materials not only reduce those risks, they also unlock premium positioning with consumers and retailers who want to feel that their everyday purchases are not actively harming the future.

The outcome is not a plastic-free world, but a world where plastic must justify its presence. When a cheaper, cleaner alternative exists, plastic will be taxed, regulated or simply refused by customers who have better options.

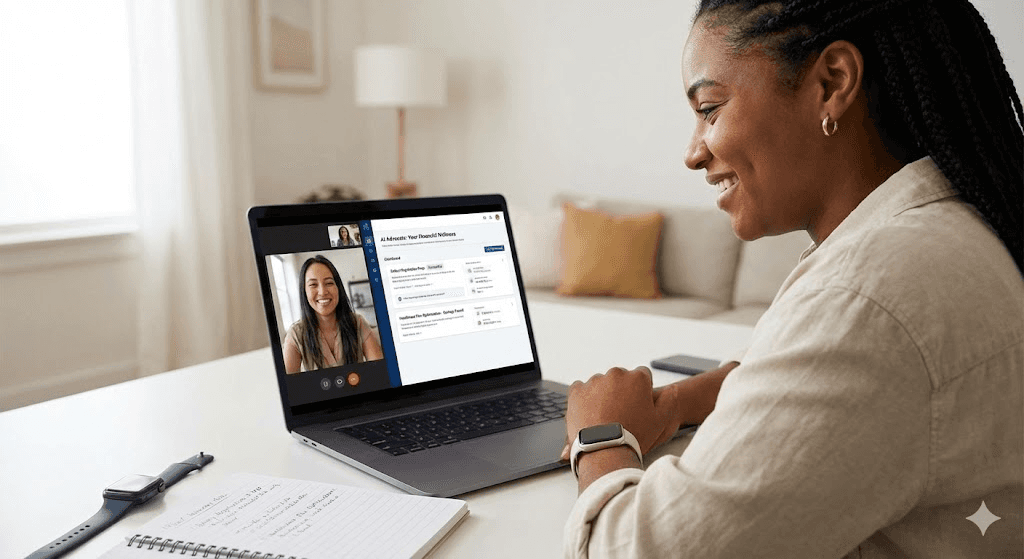

5. The Winning AI Business Model Invests In Humans

Most of the headlines in AI will continue to follow the same script: bigger models, larger data centers, new benchmarks. Trillions in capital will chase raw capability. Yet the most important business model innovation will not be about who has the largest model, but about who uses AI to serve the person on the other side of the screen.

The killer AI app is not automation, it is advocacy.

The winning companies in AI treat the individual as the client, not the product. They build personal AI agents that act like digital fiduciaries, working only in the interest of the user rather than advertisers or third parties. Personal data is stored in encrypted vaults controlled by the individual. Access is granted on the user’s terms, for specific purposes, and revocable. The business earns money not from selling attention, but from sharing in the value it helps create.

Practically, this looks like AI that coaches people into better jobs, negotiates prices on their behalf, protects their time and nudges them toward healthier, more prosperous lives. If your income rises, your stress drops or your skills compound, the AI provider gets paid. If the system sucks you into doomscrolling and mindless consumption, it has failed at its job. This is the opposite of today’s ad-driven platforms, which benefit when people stay hooked and distracted.

The company that cracks this alignment might not be one of the current giants. Incumbents are locked into attention and ad models, as well as massive infrastructure bets they must amortize. That makes it very hard for them to pivot to a world where the user is the customer and the metric is “net life improvement” instead of “time on site.” A challenger that starts with user alignment can move slower on raw capability and still win on trust.

By 2030, the most valuable AI brands will be those that people describe in personal terms: “This system changed how I work, learn and make decisions.” When users feel that AI is on their side, they will not need much convincing.

6. From Locked-In SaaS To Usage-First Software

AI is quietly attacking the foundations of the classic SaaS business model. Subscription pricing was built for a world where software was hard to learn, expensive to rebuild and painful to migrate. As AI crushes all three of those switching costs, paying for unused seats starts to feel more like a penalty than a partnership.

Time-based SaaS is about to look like paying rent on rooms you never enter.

Picture source: Billingplatform.com

Usage-based pricing is the natural response. It is already standard in infrastructure and API products, and it is spreading into mainstream software as customers refuse to pay for idle access and demand alignment with actual use. That shift will accelerate between 2026 and 2030 as AI copilots make it trivial to adopt, configure and combine tools that used to require long onboarding and integration projects.

The transition will unfold in layers. Low-defensibility tools such as utilities and simple point solutions will move first, because customers can drop them overnight when a cheaper, AI-enhanced alternative appears. Mid-tier business tools follow, forced to justify every dollar of subscription with clear, measurable value. Even complex suites and platforms will eventually be priced more granularly, as buyers gain more confidence in mixing and matching smaller components.

As AI improves interoperability and code quality, a composable middle layer emerges. Instead of monolithic applications, we see ecosystems of modules that can be connected, reconfigured and swapped out with far less friction. This opens the door for millions of small producers and micro-businesses that build narrow, outcome-focused pieces of functionality and earn through usage or success fees rather than chasing giant license deals.

The endgame is outcome-based pricing. Once switching costs are near zero and component parts are cheap, buyers will ask a simple question: “What outcome did this produce?” Software that can prove it increased revenue, reduced churn, cut costs or saved time will command a premium. Software that only promises “access” will struggle.

Read more about this in my article AI is the Side Show. The Disruption of SaaS is the Real Bomb.

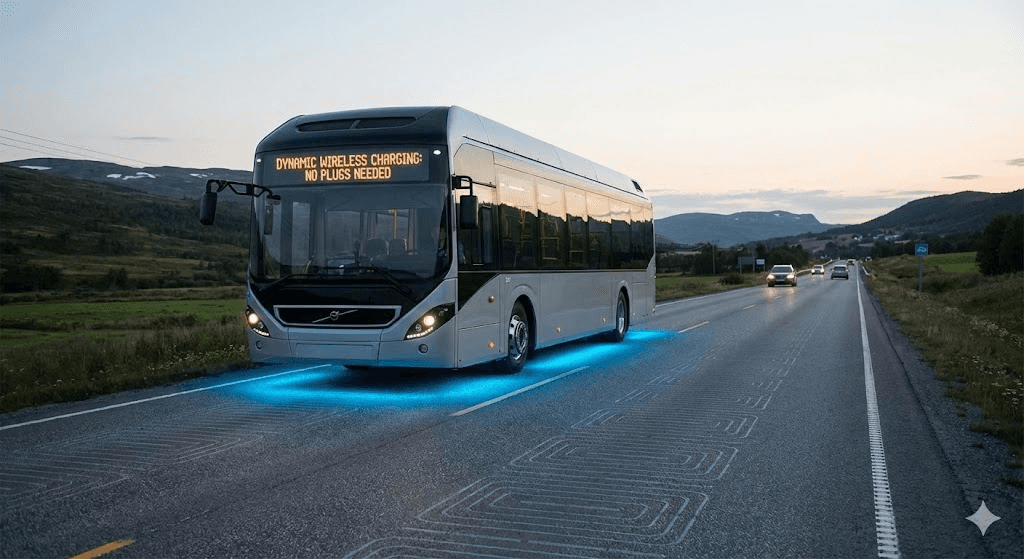

7. Endless-Energy Roads Make Plug-In Chargers Obsolete

Dynamic wireless charging on roads will feel like magic the first time people experience it. Your car simply drives, and the battery quietly refills. Underneath the asphalt, inductive coils send power to receivers in the vehicle. Range anxiety collapses, and with it the need for oversized batteries and dense networks of plug-in chargers.

The most valuable charging station becomes the lane you are already driving in.

Norway is already testing this future. In Trondheim, a 100-meter stretch of road has been equipped with inductive charging tech for electric buses, allowing them to top up while in motion and reducing the need for long charging stops. The pilot is designed to run through harsh winter conditions and to test whether wireless charging can serve as the primary energy source for public transport fleets.

If this model scales to longer stretches of highway, everything changes. Cars can carry smaller, cheaper batteries because they are not expected to store their entire journey upfront. Vehicle prices come down, weight drops and overall efficiency improves, making EVs even more competitive with combustion engines. Shared mobility and autonomous fleets benefit as well, because vehicles can stay in motion and opportunistically recharge instead of being taken out of service to sit at a charger.

For governments, the strategic value is enormous. Investing in “energy lanes” offers a way to accelerate electrification without being completely tied to the lithium and battery supply chains dominated by a few countries. It turns roads into active energy infrastructure and offers a visible, politically attractive symbol of technological progress.

Plug-in chargers will not disappear overnight, but over time they will feel more like emergency backups than the primary way to fuel an EV. Once drivers are used to the idea that roads provide energy as well as access, the idea of planning your life around charging stops will feel quaint, like asking someone where the nearest payphone is.